Don't Be Fooled - Big Banks Have Much More Risk Than Smaller Ones

By

Avi Gilburt

By

Avi Gilburt

Don't Be Fooled - Big Banks Have Much More Risk Than Smaller Ones

By Avi Gilburt and Renaissance Research

We have written quite extensively over the last several years as to why it's a huge misunderstanding to believe that the largest U.S. banks will be the safer than smaller banks in a systemic crisis scenario. If you look at the data published by various banking regulators, you’ll see that larger banks have much bigger risks than their smaller peers. Yet, for some reason, such data is often ignored by financial media, research agencies, and even independent analysts.

We’d like to remind you of some of those issues that we have been discussing in our banking work for more than two years.

Three Top-10 banks control almost 50% of total outstanding credit card loans: JPMorgan (JPM) ($181B), Citi (C) ($165B), and Capital One (COF) ($142B). In our previous article, we discussed the recent data published by the Fed. Moreover, asset quality metrics in this lending segment have deteriorated even further in the first quarter of 2024. There was a huge increase in the transition to delinquency ratio among borrowers with a 90–100% utilization rate and also quite a remarkable increase among borrowers with a 60–90% utilization rate. This implies that low-income borrowers are already in a very difficult financial situation, which looks worrisome given the reasons that led to the GFC back in 2008.

Large banks also have massive exposure to shadow banking lenders. Loans to shadow banking intermediaries and credit cards are currently the fastest-growing lending segments in the U.S. At the beginning of the year, the Fed reported that loans to shadow banking intermediaries exceeded the $1T mark. Notably, almost 70% of these very risky loans were granted by the 25 U.S. largest banks. We have published a detailed article on the topic if you are interested in further information on this issue.

Larger banks have also been increasingly buying collateralized loan obligations (CLOs) lately. A CLO is a security backed by a pool of debt. Most CLOs are backed by loans granted to private equity firms, venture capital funds, and corporations with low credit ratings. The banks disclose CLO-related data in Schedule HC-B of the Form Y-9C filing under the line "structured financial products backed or supported by corporate and similar loans." As of the end of 2023, JPMorgan had $60B of structured financial products backed by corporate and similar loans. The $60B is a significant amount, even for one of the largest U.S. banks, given that it is almost 20% of its total equity. The second-largest holder of CLOs is Citi, which had $29.7B of these securities as of the end of 2023, which represents 16% of Citi's total equity. The third-largest holder is Wells Fargo (WFC), which had $29.4B of these securities as of the end of 2023, which corresponds to 14% of Wells' equity. We have also discussed these issues previously.

Believe it or not, there are more major issues on larger bank balance sheets, which we have covered in past articles. And, when you consider that there was one major issue which caused the GFC back in 2008, we currently have many more large issues on bank balance sheets. So, in our opinion, the current banking environment presents even greater risks than what we have seen during the 2008 GFC.

In this article, we would like to discuss two even further worrisome facts that have been recently revealed by the FDIC.

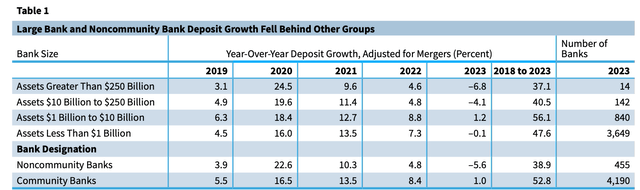

The table below shows a breakdown of deposit dynamics based on the banks’ asset sizes. As we can see, the popular narrative that “the largest banks saw huge deposit inflows due to the SVB collapse in 2023” is wrong. In fact, the banks with assets of more than $250B posted the biggest deposit outflow.

FDIC

We also note that smaller community banks saw an inflow of deposits. This also refutes what many are saying about deposit issues at community banks. Here is a formal definition of a community bank, which was provided by the FDIC.

"Community banks are smaller institutions, generally under $1B in total assets, with a business model focused on a limited geographic area."

Almost all the banks that we have recommended to our clients are community banks, which do not have any of the issues we have been outlining over the last several years. Of course, we are not saying that all community banks are good. There are a lot of small community banks that are much weaker than larger banks. That’s why it is absolutely imperative to engage in a thorough due diligence to find a safer bank for your hard-earned money. And, what we have found is that there are still some very solid and safe community banks with conservative business models.

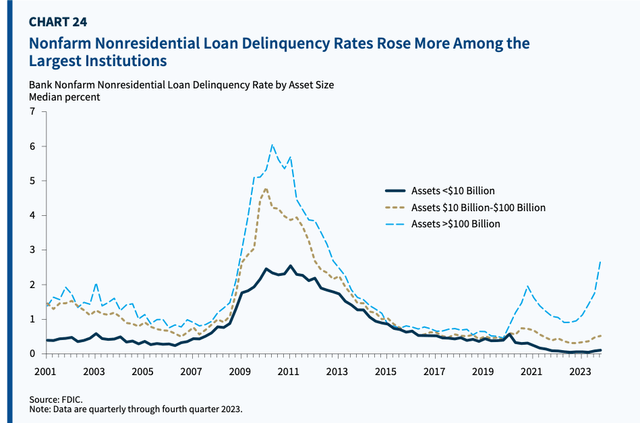

Another thing that caught our eye is the FDIC’s data on CRE loans. The chart below shows that the largest banks (assets > $100B) posted the sharpest increase in the CRE loan delinquency ratio. This shows that another popular narrative that “only smaller regional banks will face CRE-related issues” is also wrong.

FDIC

The FDIC also adds that an estimated $1.6T in CRE loans will mature between 2024 and 2026. More than half of these maturing CRE loans are held by banks and are predominantly loans to finance nonfarm nonresidential properties, which include office loans. Importantly, large office loans (loans over $100MM), which are obviously mainly granted by bigger banks, had the lowest refinancing success rate among CRE loans in 2023. This suggests that larger banks will likely face very significant issues in 2024–2026, when these large office loans will need to be refinanced.

Bottom line

In this difficult environment, you should take most stories from the financial media, analytical reports, or even articles by independent analysts with a very large grain of salt. A lot of the conclusions from these reports are incorrect and not supported by the public data. We would not rule out that a very powerful banking lobby has a role in that.

So, I want to take this opportunity to remind you that we have reviewed many larger banks, including the three just noted, in our public articles. But I must warn you: The substance of that analysis is not looking too good for the future of the larger banks in the United States, and you can read about them in the prior articles we have written. And, as these issues get worse, the risk continues to rise.

Moreover, if you believe that the banking issues have been addressed, I think that New York Community Bancorp, Inc. (NYCB) is reminding us that we have likely only seen the tip of the iceberg. We were also able to identify the exact reasons in a public article which caused SVB to fail, well before anyone even considered these issues. And I can assure you that they have not been resolved. It's now only a matter of time before the rest of the market begins to take notice. By then, it will likely be too late for many bank deposit holders.

At the end of the day, we're speaking of protecting your hard-earned money. Therefore, it behooves you to engage in due diligence regarding the banks which currently house your money.

You have a responsibility to yourself and your family to make sure your money resides in only the safest of institutions. And if you're relying on the FDIC, I suggest you read our prior articles, which outline why such reliance will not be as prudent as you may believe in the coming years, one of the main reasons being the banking industry's desired move towards bail-ins. (And, if you do not know what a bail-in is, I suggest you read our prior articles.)

It's time for you to do a deep dive into the banks that house your hard-earned money to determine whether your bank is truly solid or not. You are welcome to use our due diligence methodology outlined here.

This article, as well as Saferbankingresearch.com, is a combination of efforts between Avi Gilburt and Renaissance Research, which has been covering U.S., European, LatAm, and CEEMEA banking stocks for more than 15 years.